Your children may not be walking (or perhaps not even born yet) but you’re already wondering how you’re going to pay for their education. If you’ve started the research process, you’ve probably come across a 529 plan, and wondered if it’s a viable option.

As a physician, you have many choices for saving for your child’s education. Sure, you could utilize a traditional savings account but there are many other alternatives which could potentially provide more bang for your buck.

And we have to be realistic about the cost of college now. We’ve all heard tuition is on the rise, and it doesn’t appear to be getting lower anytime soon. The average cost for a private, four-year bachelor’s degree is over $48,000 on an annual basis.

If you don’t want to have to practice medicine until you’re 95 years old in order to pay for your children’s education, then you’re probably interested to know all the opportunities available to you.

Let’s address 529 plans, so you can decide if this is an appropriate tool for you to use as you prepare to pay for education.

The Basics of a 529 Plan

The Basics of a 529 Plan

A 529 plan is also referred to as a “qualified tuition plan.” The term “529” comes from the 529 section of the IRS code. The program began in 1996 as a way for you to set aside after tax dollars for education expenses, but allow the money to grow tax-free.

The plan was developed as a way to encourage savings for education, while receiving a potential tax advantage. Once you choose to invest, the growth on the plans is tax-deferred for you.

Basically, it’s a savings account for education.

You deposit money into these state sponsored plans (or education sponsored plans, whichever you choose) and you are essentially investing the money. All earnings you make off of the growth is yours to keep to cover for specific education costs.

You can eventually withdraw the money and use it to cover expenses related to most secondary school expenses. Expenses such as tuition, room and board (both on and off campus), books, equipment, supplies, even the internet. There are also qualifications for the purchase of computer equipment.

Since the 529 plans are offered by each state, the state usually offers income tax credits and tax deductions to those who contribute. And speaking of contributions, it only takes a small amount to start contributing. In some cases, the state plan requires as little as $10.

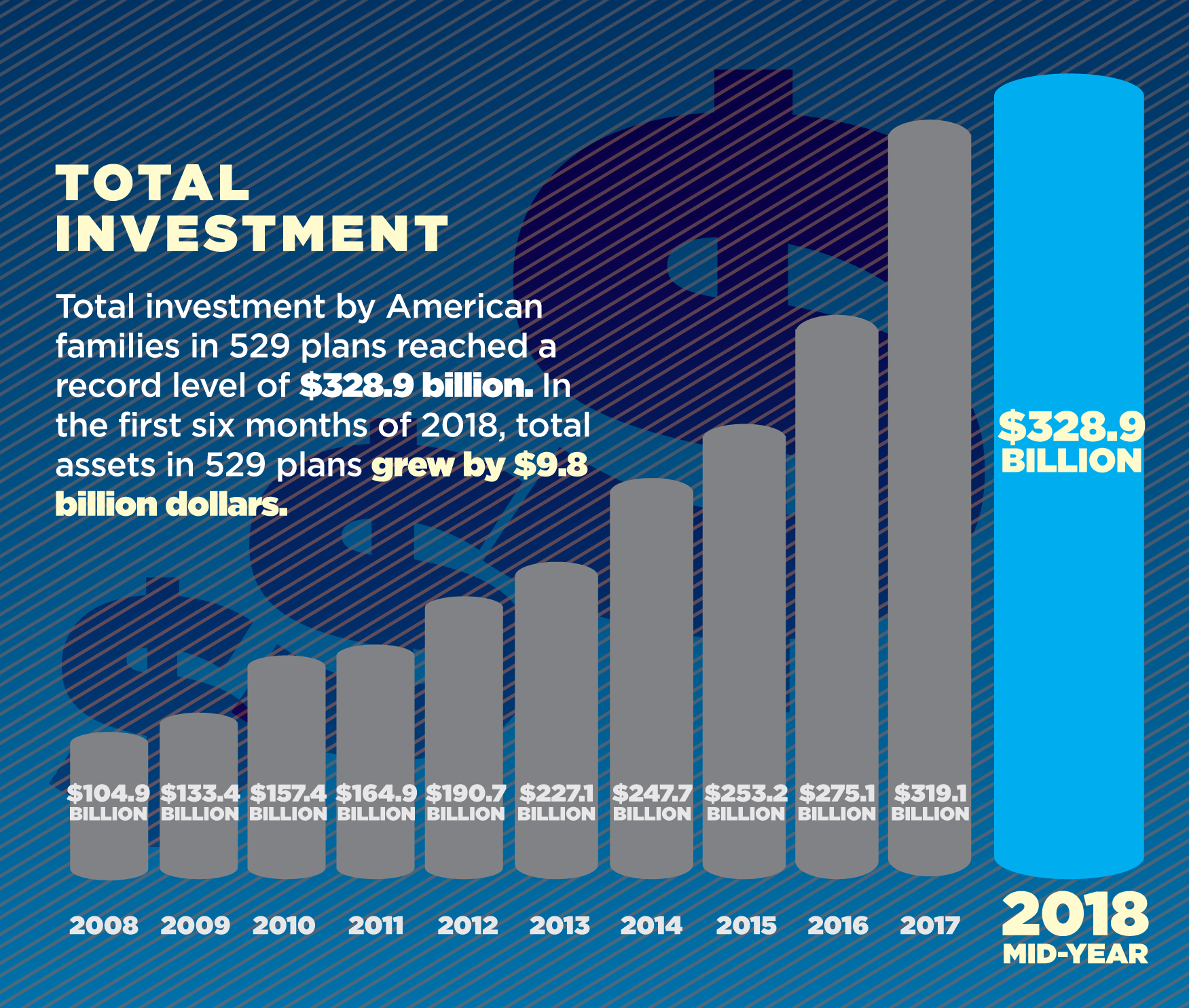

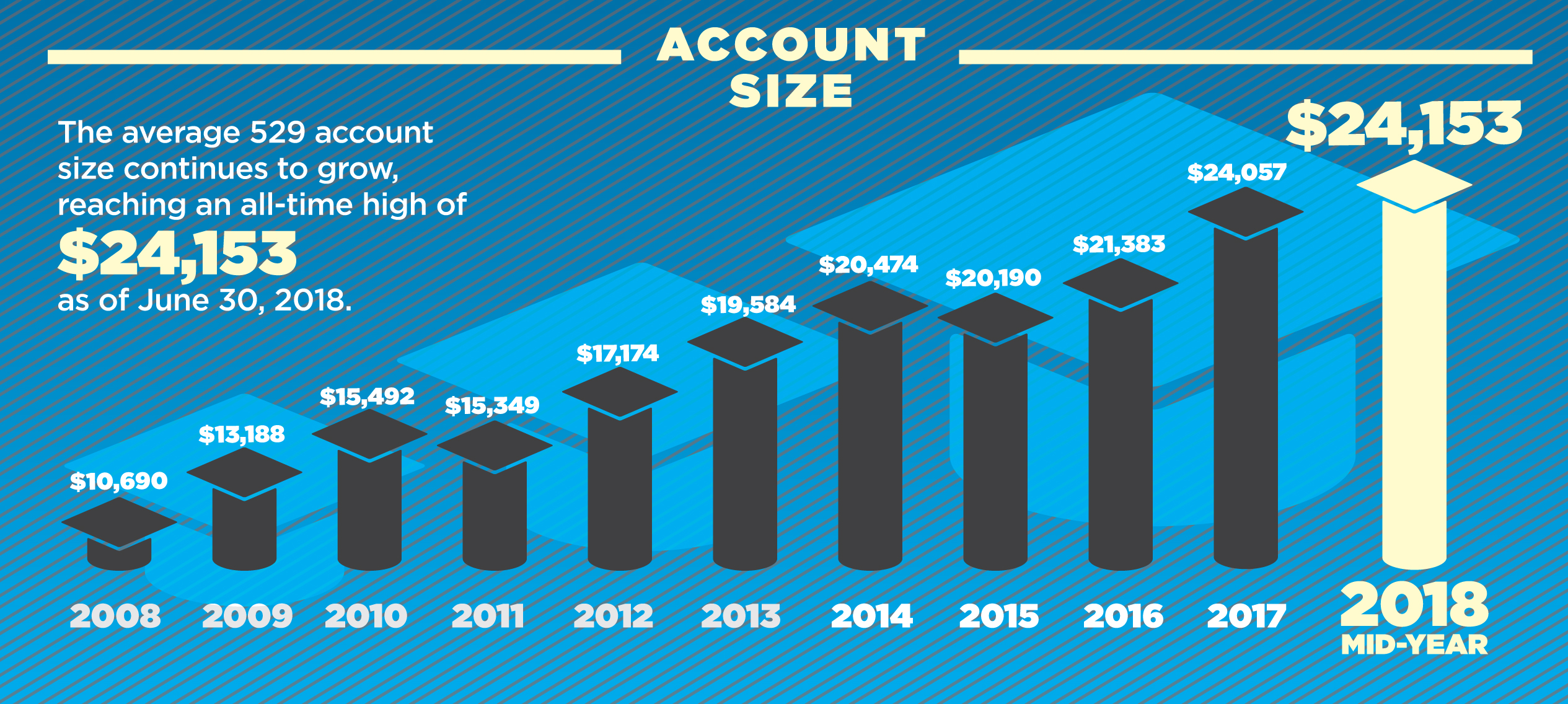

The 529 plans have become increasingly popular since their inception, and it doesn’t appear to be slowing down anytime soon. As of June 2018, a record $328.9 billion in contributions were made towards the 529s, just in the first half of 2018. The average amount in a 529 has reached a record of over $24K per account, too.

The Benefits of 529 Plans

Over the years, as the 529’s have continued to gain popularity, there have been several tweaks to the program. As a result, there are multiple benefits to the 529 plans.

Since you can open an unlimited number of accounts (for each of your children or for multiple relatives), you need to know how this program can help you pay for education.

Not Just Limited to a 4-Year Degree Program

The 529 plans can actually be used to help for whatever type of education your child chooses after high school graduation – it’s not limited to the traditional 4-year school or degree.

Funds from the 529 plans can go towards a 2-year school, a graduate program, a professional degree, or a vocational school.

There is a large number of eligible institutions within the United States – currently over 4,000 for you to choose from.

In some cases, the 529 plan can be used to offset the costs of a study abroad program. You can travel to Europe for instance, and use the funds to help pay for the program. The funds from the 529s can also be applied to continuing education courses, if the institution is one on the eligibility list.

As of 2018, you can actually use the 529 plan towards the cost of other types of education expenses. You can now use up to $10,000 per year “ for tuition in connection with enrollment or attendance at an elementary or secondary public, private, or religious school,” per the IRS.

This new rule allows you to withdraw an amount if you need it, during your child’s K-12th grade years. You are no longer limited to post-high school education with the 529 plans. If you do choose to use the funds for your child’s K-12 years, just keep in mind you are missing out on potential years of compounding interest.

Tax Benefits

Tax Benefits

Although your actual contributions do not qualify as a tax deduction, there are other tax benefits which can be utilized by setting up a 529 plan.

From a federal tax point of view, the earnings on these accounts are not subject to federal income taxes. It’s pretty simple, really. Your money grows tax-free and you are not taxed on the withdrawal, when it falls within the education guidelines.

In addition to the federal tax benefits, you could be entitled to additional state benefits. Currently there are 30 states, in addition to Washington D.C., which offer some sort of tax benefit if you are enrolled in a 529 plan.

If you live in Arizona, Arkansas, Kansas, Minnesota, Missouri, Montana, Pennsylvania then the news gets better. These states offer a tax benefit to any 529 plan you contribute to, even if the plan wasn’t setup in one of these 7 states.

You Choose Where to Invest

With the 529 Plans, you are in complete control. Not only are you the full custodian of the account, but you can also select which state you would like to open an account in.

Yes, that’s correct! You can open an account in any state, and it doesn’t have to be the one you reside in either. You can select the state which best represents your goals and what you want to achieve for taxes and credits.

Not only can you open an account in any state which offers a 529 plan option, but the beneficiary of the plan does not have to attend an institution in the state you have selected.

As you begin your research, you will want to take a look at the various advantages of certain states, and how you can benefit the most. You could find you’re better off choosing a state where you have a higher chance with future earnings versus investing in a plan with your home state – even with a tax benefit.

In addition to choosing the state, you can choose which plan your money is invested in. You can pick and choose specific investments for your contributions.

You can also choose plans based on the age of your children. If you have young children and start contributing when they are little, then you can choose to pick funds which are considered “more aggressive.” The older the child is, then you can research plans which may be considered more conservative.

You will have the choice 2x per year to make changes to your plans, or if you need to make a change to your beneficiaries. Ultimately, this provides a great level of flexibility.

You Can Transfer Your Benefits

You Can Transfer Your Benefits

So what if your child decides not to go to any type of college? Or, what if you have one child and they end up receiving a full scholarship to pay for college? Maybe you end up deciding not to have children – there are many scenarios which could play out.

The good news is, you can transfer the amount to any relative without consequence. This also includes yourself, should you want to further your education. You can simply change the beneficiary on the account and you can do so without incurring a penalty.

And as far as relatives are concerned, you can change the beneficiary to anyone as far out as your first cousin.

You can also withdraw your funds if you end up not needing them whatsoever. Although you will face a tax penalty (currently you pay a 10% tax penalty as well as capital gains on the growth) the money is yours to withdraw.

If your child (or children) receive full scholarships and you no longer need the funds, then the 10% penalty fee is waived.

Other Considerations With 529 Plans

There are many potential benefits to these plans, but before you go down the path of a 529, you want to make sure you have complete understanding.

Penalties for Withdrawing Funds

As mentioned earlier, there is a 10% withdrawal penalty, should you choose to take your money out of the plan and use it for non-educational expenses. Remember, the 10% penalty will occur on the earnings, not the aftertax dollars you contributed.

The only time the 10% penalty is waived is if your child receives a scholarship, or if the beneficiary dies or is disabled.

Be Careful With Non-Qualified Expenses

It’s important to note, the new rule allowing up to $10,000 per year for the K-12 tuition allowance, is for tuition only. You can not use the amount for anything other than tuition, no matter if it’s related to an educational expense or not.

However, with the post- high school plans, you can use the funds for all educational related expenses, as mentioned earlier.

Be Aware of Contribution Limits

Each state has a different amount for limits on contributions to the plan. It’ll be important for you to know the details, depending on which state you end up selecting.

The limits are pretty generous though – it’s not unusual for plans to have around a $300K maximum, per beneficiary.

Get Help if You Need It

Many financial advisors can help get you setup for the 529 plans. Of course, along with the guidance of a financial advisor, you will also have fees to pay.

If you don’t want to utilize the help of a financial advisor, you can always purchase a 529 plan directly from the state you have selected.

Other Ways to Contribute to the 529 Plans

There’s nothing set in stone which says you have to withdraw several hundred dollars from each paycheck to fund the 529 plans.

Whenever your child’s birthday or a special occasion rolls around, ask the grandparents or aunts and uncles to contribute to the child’s 529. A $25 contribution, while they’re young, can really add up over time.

Even your friends can contribute! Don’t be afraid to let them know if they are asking for your input.

Not only does the 529 accept checks made out to the account, but there are also options available to purchase gift cards. These gift cards are found at most big retailers, which makes it easy for people to contribute.

You don’t even have to open the account for your own children. The grandparents (or any other relative) can open the account. Just keep in mind the person opening the account is the one who receives the tax benefits.

When to Invest in a 529 Plan

Of course it’s ultimately up to you to decide if and when to start investing in a 529 plan. I work with many physicians who want to know when the best time to start investing in education is.

But one piece of advice I always offer to my clients is to make sure their financial house is in order before you contribute to a 529 plan.

As much as we want to help our kids out in any way possible – which includes their education – you should try to have your other financial priorities defined as well, and be working towards your plan.

Monthly Budget is in Place

Before you make any decisions, you need to be committed to the idea of a monthly budget. Do you know how much you have coming in each month, and more importantly, how much you have going out?

Developing a budget is a smart strategy in your overall financial game plan. There are plenty of tools to help you develop the one which is right for you, if you need help getting started.

Emergency Fund Is Loaded

Emergency Fund Is Loaded

If you have hung out here on Financial Residency for any amount of time, you know I like to talk about the importance of a fully funded emergency savings. If you are having a hard time setting aside 3-6 months worth of savings, then you need to focus on this first, before the education.

We all know emergencies never happen at a convenient time. Whether you’re a resident or full attending, having 3-6 months of your salary set aside means you have a financial safety net.

You Are Tackling Debt

If you are still carrying a heavy burden of student loan debt, then it’s time to consider what you can do to ease this debt. The same goes for credit card debt – you should get out from under the drag of debt before you start contributing to a college fund.

Most likely as a physician you’ve experienced your fair share of student loans. It makes you painfully aware of how much the cost of education can impact your monthly spending, long after you’ve earned your degree. It could be the motivating factor for wanting your child to not have to worry about tuition expenses.

Whatever the case, you have to get a plan to tackle the debt before you fund someone’s education.

Fully Funding Retirement

Another area you want to make sure you’re fully funding is your retirement savings. Are you contributing as much as possible from your hospital’s 403(b) plan? If not, could you go ahead and make an adjustment before you think about college?

Are you contributing to an IRA? If your workplace doesn’t offer a retirement option, you can always fund an IRA.

Once you have these major areas of your finances planned out, then it’s time to start seeing how contributing to a 529 plan can fit in your overall financial roadmap.

All of this being said, you will see the most benefit if you can start contributing to the 529 early in your child’s life. Since you are depending on the growth of the account, it makes the most sense to give it as much time as possible to grow.

A 529 Plan Can Be a Helpful Tool

What are your thoughts? Is a 529 plan worth the effort to research and setup? There are definitely a few tax advantages which deserve consideration as you plan for the future. But also keep in mind, it doesn’t have to be the only way to save for your child’s education.

A 529 plan could end up being one of many avenues for you to pursue with savings. If you still have questions or want to explore all of the options available for physicians, then it could be a good time to setup an appointment with your fee-only financial advisor.

{kind=link}

{kind=link}