Saving for college is a monumental task. The savings aspect alone is enough to warrant questions, debates, and discussions with your family and financial advisor.

The questions are plentiful.

- How do you know how much to set aside?

- How much higher can the cost of college continue to climb?

- How do you know for sure your child will even attend college?

These are all valid questions as you start to make real decisions for your child’s future. And for physicians, the decision is just as difficult.

Sure, you will be making a great salary (if you aren’t already) and have a steady income. By the time your kids go off to college, you’ll presumably be well-established in your practice with a consistent, dependable salary to match.

But this doesn’t mean you want to “wing it” when it comes to saving for such a big milestone in your child’s life either. You’re wondering what you can do right now so you can be in the best position possible in 5, 10, or 15 years down the road.

As a financial advisor, I’m asked a great deal about the right way to save for college. A common question is whether to tap into a whole life insurance policy or set aside funds for a 529 college savings plan.

Today we want to consider the pros and cons of using whole life insurance vs. 529 college savings plan for future education. Let’s see how these two options compare to one another.

Why Save for a College Education?

Let’s start with the very basic idea of why saving for education should be considered. Yes, paying for your child’s education is a personal decision – and not everyone is convinced of the need to save.

But with rising tuition costs and with so many options available to students these days, there is also something to be said for setting aside funds for the future. You may (or may not) be surprised to learn that tuition continues to increase at staggering amounts each year. The latest estimates show an in-state public school will cost an average of $19,000 per year. This is almost a 3% increase in only one year.

If private school is the path your child wants to choose, then get ready for even more of a sticker shock. Private tuition is hovering around $35,000 annually. The $35,000 is also up over 3% versus the prior year.

The bottom line, college tuition isn’t cheap.

We can’t anticipate costs shrinking anytime soon, so now it’s time to figure out smart ways to use our money so the tuition costs don’t sting quite as much.

Pros of Using a 529 Plan

The 529 plan is a fantastic vessel for savings when it comes to education. Like many other investments, the sooner you can begin contributing, then you’ll reap the full benefit. But if you’re going to compare whole life insurance versus a 529 plan, then you need to know how each can benefit you.

At its very basic definition, a 529 plan is a savings account for educational expenses. There are several states (30 to be exact, including Washington D.C.) which sponsor a specific plan for 529s. You deposit the money into an account, and the state will invest it for you. You will then have access to the funds, including any earnings you may realize.

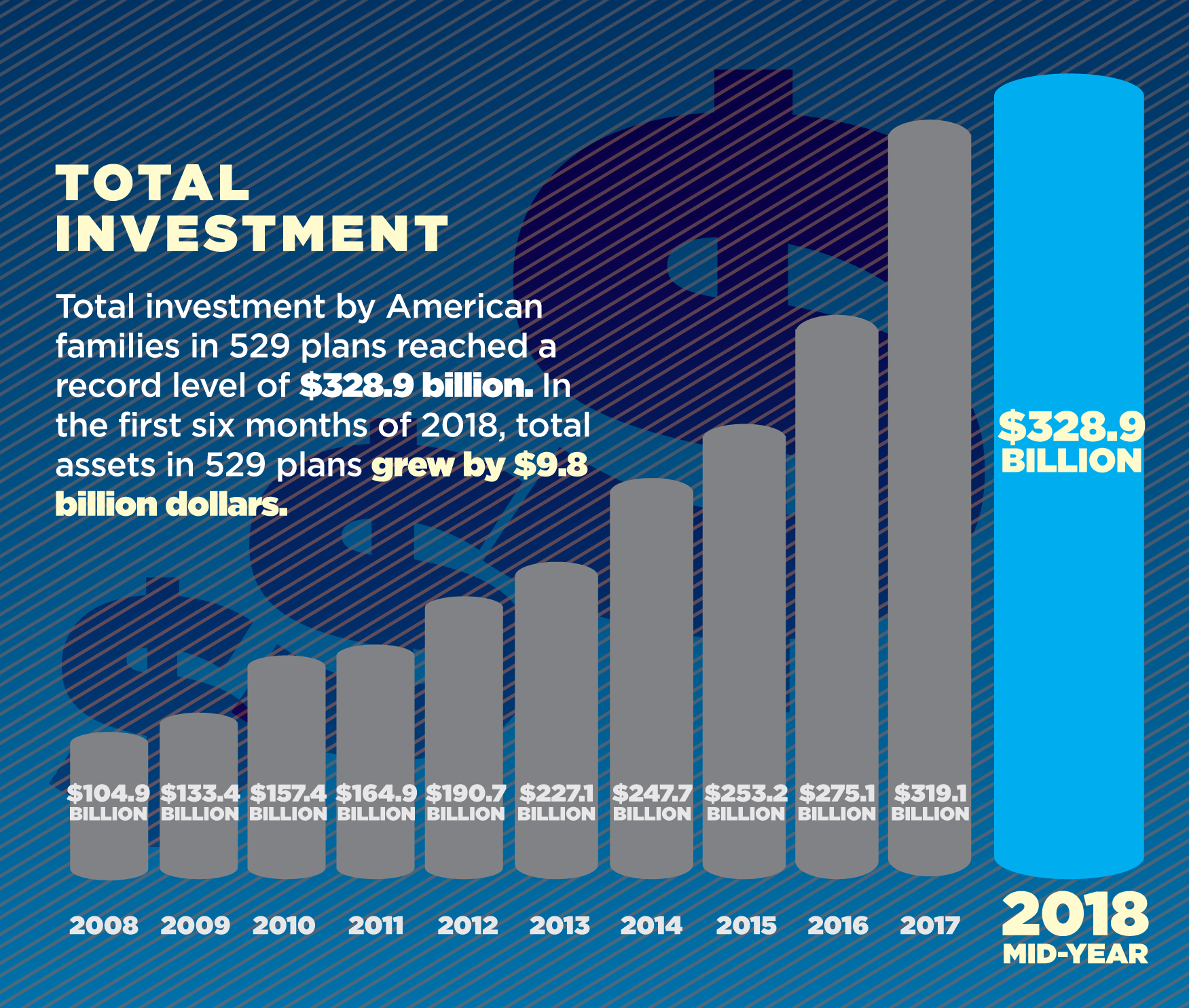

What’s important to know about 529 plans is they are investments – which means they come with a certain level of risk. However, the 529 plans have become a very popular choice and there is continued growth each year.

You can open as many of the accounts as you choose, which is perfect if you have more than one child.

What exactly are the advantages to the 529? Luckily there are quite a few for you. You will see not only are there multiple advantages, but there is a great amount of flexibility with a 529.

Tax Advantages

There are tax advantages associated with contributing to the 529 plans. When it comes to Federal taxes, the earnings on the 529s do not get counted as income for you. Your money is allowed to grow tax-free, assuming you’re contributing and withdrawing within the stated guidelines.

In addition to the federal tax benefit, several states offer additional tax benefits. There may be a benefit on the earnings or the actual contribution. Each state plan can have a variation to it.

Low Fees

There are very few fees associated with opening an account. As a matter of fact, if you choose to open the account yourself, then you shouldn’t be charged any amount with the opening.

There are fees associated with using a financial advisor to open the account for you. There are also fees associated with withdrawing the funds for non-educational purposes.

Unlike whole life insurance plans, you won’t be subject to hefty yearly fees on the accounts. Currently, whole life insurance plans are sitting around 2% in yearly fees. Most state plans are free each year. There is a handful which charges a $10-$25 annual fee for the 529 plan. This makes for a nominal yearly charge to maintain a 529 account.

You Can Shop Around

Each state has its own program – and advantages – for contributing to a 529. Yes, it’s worth the time to research which of the 30 states may have the best plan for your situation.

You are free to choose whichever state’s plan you prefer – no matter if you’re living in that particular state or not. Currently, there are 7 states which offer a double incentive if you invest in their 529 and are a resident (Arizona, Arkansas, Kansas, Minnesota, Missouri, Montana, Pennsylvania – in case you’re wondering).

When you’re shopping around, you want to consider which state’s plan has the most potential for future earnings. You also need to weigh the tax incentives, even if there is a higher earning potential. You can easily find out which state is producing the highest earnings with their savings plans, based on a year (or several) years of data.

You can also choose a different state’s plan for each account you have. If you have an older child which you’ve just started to save for, then you may choose a different account compared to what you would purchase for a very young child. In this example, you could choose a state whose plan is more aggressive and can earn more in a shorter time period.

If the thought of spending hours researching the various state’s plans makes you want to scream, then you can also seek the help of a financial advisor, and preferably a fee-only advisor. They can assist you in picking the best plan (make sure to confirm the fees associated with this) based on your preferences.

You Can Start Off with a Very Small Amount

You’ll be happy to know you can open an account for as little as $10 in some states. You should confirm the opening contribution amount with the state’s guidelines you open the account with, but typically the threshold is quite low.

This could be especially appealing if you’re still in your residency, living on an extremely tight budget. If you want to get a head start on saving something, then you don’t have to worry about having a large lump sum in order to get started.

Can Be Used for More Than a 4-Year Degree

529 plans not only offer low fees and a small cost of entry, but the funds can be used for other aspects of education besides a 4-year degree. The 529’s can be used to help pay for any post-secondary education, which includes technical colleges, 2-year schools, or graduate work.

A newer change to the 529 program is the ability to use the funds for private education for elementary and/or secondary education. You are allowed to use up to $10,000 per year towards a private school. It can be used towards a religious or non-religious school, as long as it’s K-12 and you use it for tuition only.

There are currently over 4,000 institutions which qualify as eligible to use your earnings towards. Chances are high the post-secondary choice of your child will be eligible for the funding from a 529 plan.

Friends and Family Can Contribute

We all know grandparents and other family members love to buy impractical gifts for your kids – it’s almost a rite of passage. However, if your family members ever ask your opinion on a gift, then encourage them to contribute to a 529 plan.

Simply adding $25 to the account each year can make a meaningful difference over the life of the account. Contributing to a 529 plan is an easy way for everyone to get involved with helping towards the cost of education.

You will now find several mass retailers who carry gift cards which can be used to contribute to a 529. Your kid might not appreciate the gesture as much as you do, but the gift cards make it even easier (and convenient!) to add money to the plan.

If You Don’t Use it, You Don’t Lose It

One of the best features of the 529 plans is the fact you aren’t dinged too heavily if your child chooses not to go the college route. There is a great amount of flexibility with the savings, should your needs change over the years.

For instance, let’s say you have more than one child and your oldest decides not to attend college. You can easily transfer the account to one of your other children who may choose to pursue post-secondary education.

If you don’t have any other children, then you can transfer the savings to yourself and use it for your own continuing education. Or you can choose to give it to another family member who is in need. You can extend it to both immediate and some of the extended members of your family.

Worst case scenario, no one in your family (including you) ends up using the funds from the 529 plan. You would have to pay a 10% penalty on the growth of the funds in the account. This could be considered a minimal risk you’re willing to take.

Many people are concerned about the penalty to withdraw if your child ends up getting a scholarship. If your child (or all of your children) have earned scholarships and do not need the 529 funds, the fee is waived.

The Possibility of Using a Whole Life Insurance Policy

If you have already chosen a whole life insurance plan, then you need to know your options available with your policy. Tapping into a whole life insurance policy could be a consideration if the policy has been in place for several years.

But be warned. If you choose to use the cash value of your policy to help fund a college education, you need to make sure you understand the fees associated with withdrawal. There could also be a potential tax penalty if you withdraw from your policy prior to age 59 ½.

Borrow Against the Death Benefit

There is a way you can borrow against your death benefit with your whole life insurance policy, in order to fund college. Your whole life policy may have built up a cash benefit, depending on how many years you’ve had the policy.

By using the money against the death benefit, you can either choose to pay it back or your agent can simply deduct what you need to withdraw from the payout upon death.

Policy Is Not Factored in Earnings

If your child is applying for financial aid, whether it’s in the form of a scholarship or student loans, then a whole life policy will not be used to calculate parental assets. This is where the 529 differs because a 529 will be taken into consideration with the applications.

Will Not Incur the Penalty If Child Doesn’t Attend a Post-Secondary School

As mentioned earlier, with a 529 plan, you will be subject to a penalty if the funds end up not being used and you choose to withdraw them for non-educational purposes. Obviously, if your plan is to use your whole life policy and you end up not using it, then you don’t have to worry about incurring a penalty.

But giving advice on how you can use whole life insurance to help finance an education shouldn’t be perceived as an endorsement for obtaining whole life insurance. As a fee-only financial advisor, we always advise our clients to consider a term-life policy instead of whole life insurance. However, it’s likely some of you already have a whole life policy in place and you are wondering what your options are for post-secondary education.

When to Start Saving

As with almost every financial decision we are faced with, the sooner we can put our plans into place, the better. There are other things you can do so you don’t have to solely rely on a whole life insurance policy or a specific type of savings account.

There are several steps you can take to prepare yourself financially long before your child’s first year away at school – and it’s not limited to opening a 529 plan or any other account.

Yes, there are steps such as paying off your consumer debt and mortgage, eliminating your own student loans, and managing a monthly budget. All of these financial milestones can help you contribute to paying for college as the tuition bills start coming in. You’re essentially able to “cash-flow” the education costs and add it to your monthly budget.

As tempting as it is to want to start saving for a 529 right away, or potentially look into using a whole life policy, you want to make sure your finances are healthy overall. Once your finances are in order, then you can make a solid plan to contribute to your child’s education, without risk to your current financial circumstances.

Whole Life Insurance vs. 529 College Savings Plan: The Bottom Line

When you look at the facts, whole life insurance versus a 529 plan for a college education is a straightforward scenario. There are very few reasons I would recommend someone to have a whole life policy in the first place, let alone use it towards college. Between the two options, a 529 plan offers several benefits.

With today’s multiple options for contributing to 529 plans, it makes it a great choice for setting aside funds. A 529 plan is one of the many tools available to you for saving and investing for your child’s future education. By using a 529 plan, you’re not subject to hefty fees and you have several options to maximize earnings.

{kind=link}